Plan Your Loan Repayment - Complete Loan Calculator Guide

Understand the difference between equal payment and equal principal repayment methods. Learn how to accurately calculate loan interest and monthly payments.

Know Your Loan Before You Borrow

"How much interest on a $300,000 loan at 4%?" "Which is better: equal payment or equal principal?" "30-year vs 20-year loan - what's the monthly payment difference?"

Mortgages, auto loans, personal loans... loans are an inevitable part of modern life. But complex terms and calculations can be overwhelming.

Toolypet's Loan Calculator lets you input various conditions to see monthly payments, total interest, and repayment schedules at a glance.

How to Use the Loan Calculator

Input Fields

- Loan Amount: Total amount borrowed

- Annual Rate: Interest rate (%)

- Loan Term: Repayment period (months)

- Repayment Type: Equal Payment or Equal Principal

View Results

- Monthly Payment: Amount due each month

- Total Payment: Principal + Interest

- Total Interest: Interest over loan term

- Repayment Schedule: Detailed breakdown by month

Understanding Repayment Methods

Equal Payment (Amortization)

Feature: Pay the same amount every month.

- Monthly payment = (Principal + Interest) stays constant

- Early payments are mostly interest, later mostly principal

- Easy budget management (fixed expense)

Formula:

Monthly Payment = P × [r(1+r)^n] / [(1+r)^n - 1]

P: Loan principal

r: Monthly rate (annual rate ÷ 12)

n: Total months

Equal Principal

Feature: Pay the same principal every month, with interest on remaining balance.

- Monthly principal = Loan amount ÷ Total months (fixed)

- Monthly interest = Remaining balance × Monthly rate (decreases)

- Total interest less than equal payment

- Higher initial burden, decreasing payments

Formula:

Monthly Principal = P / n

Monthly Interest = Remaining Balance × r

Monthly Payment = Principal + Interest (decreases monthly)

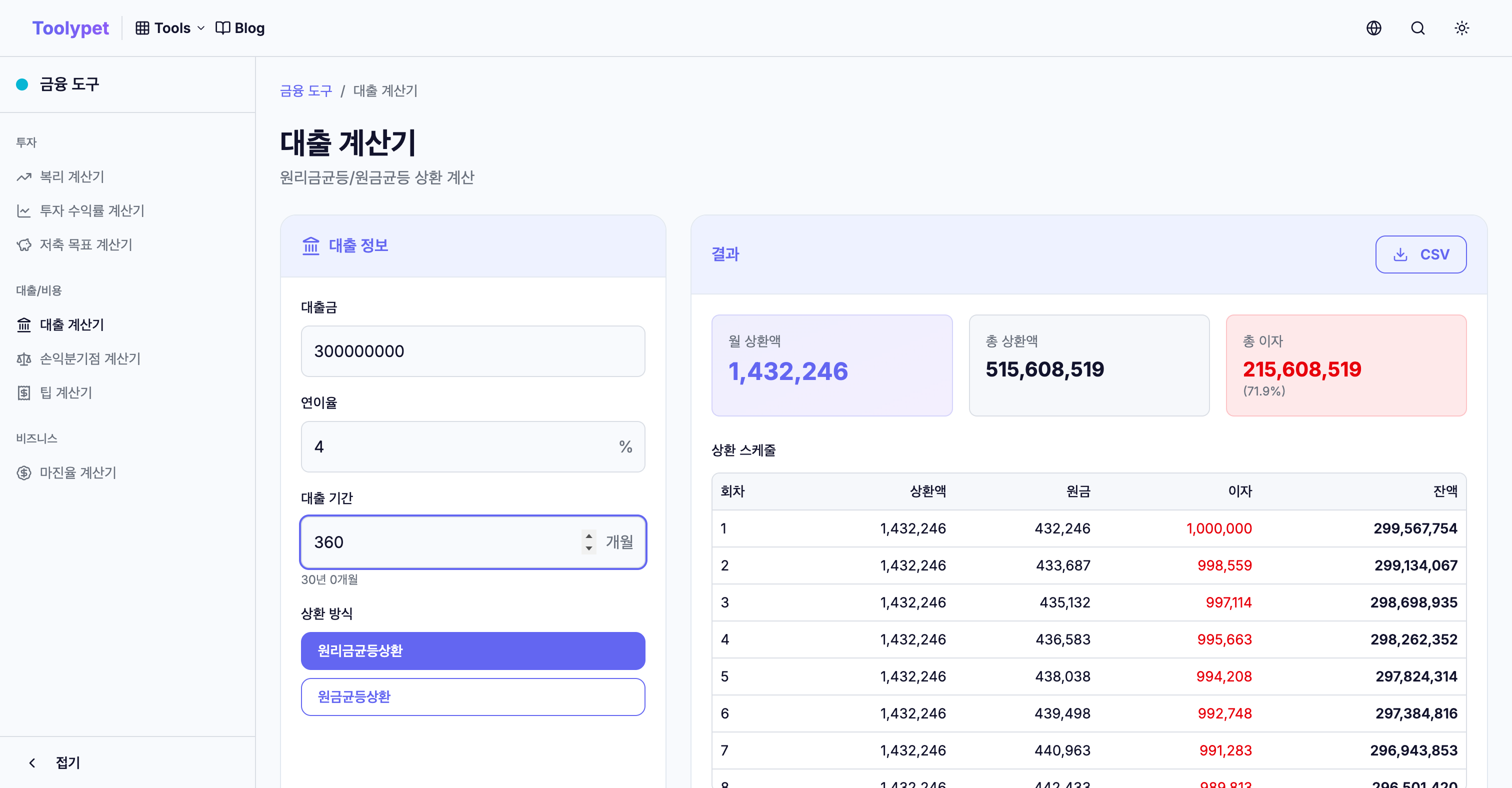

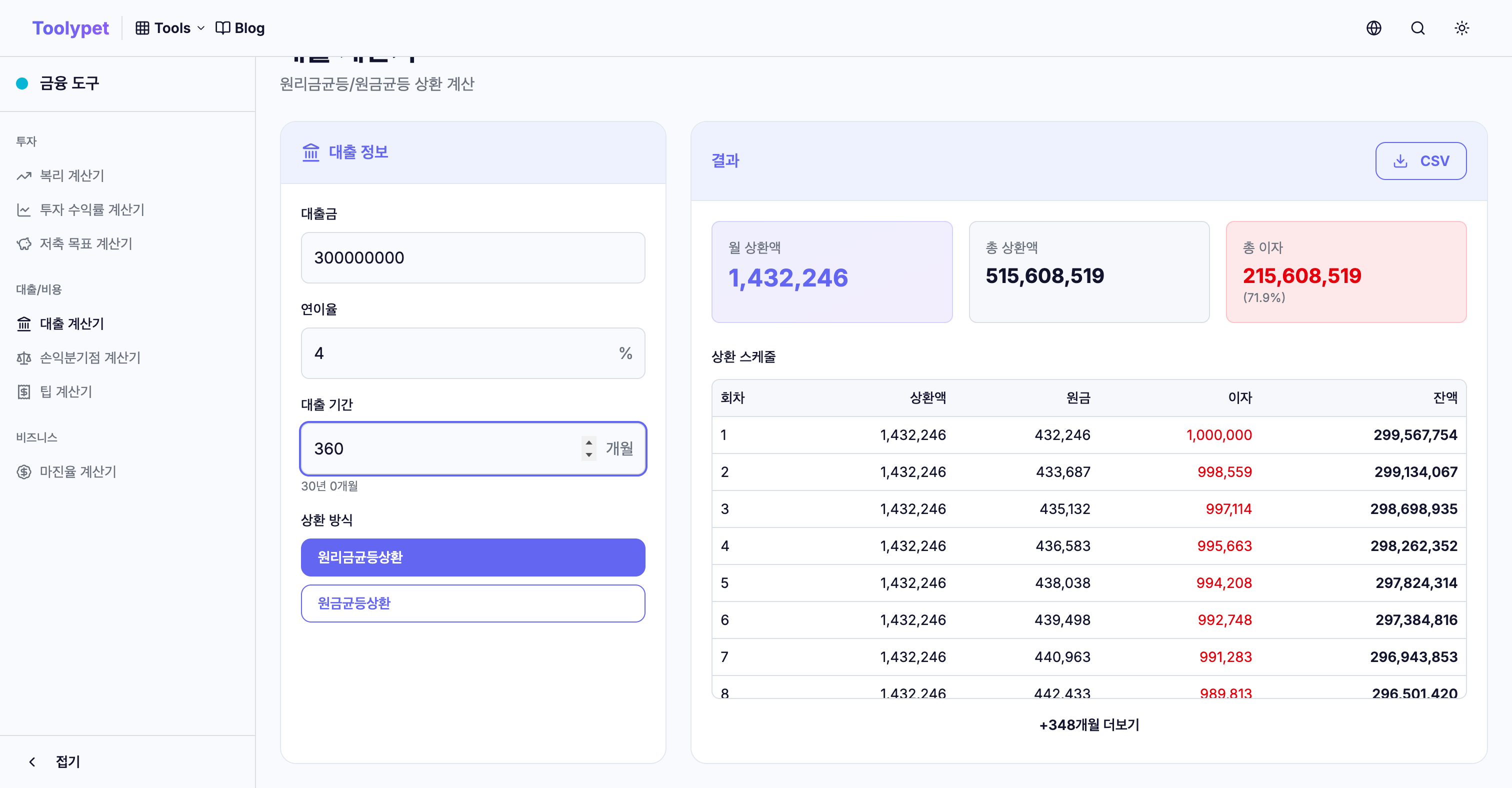

Real Comparison: $300,000, 4%, 30-Year Loan

Compare both repayment methods with identical conditions.

Loan Conditions:

- Amount: $300,000

- Annual Rate: 4%

- Term: 30 years (360 months)

Equal Payment

| Item | Amount |

|---|---|

| Monthly Payment | $1,432 (fixed) |

| Total Payment | $515,609 |

| Total Interest | $215,609 |

Equal Principal

| Item | Amount |

|---|---|

| First Month Payment | $1,833 |

| Last Month Payment | $836 |

| Total Payment | $480,500 |

| Total Interest | $180,500 |

Comparison Results

| Comparison | Equal Payment | Equal Principal | Difference |

|---|---|---|---|

| Initial Monthly | $1,432 | $1,833 | +$401 |

| Total Interest | $215,609 | $180,500 | -$35,109 |

Equal principal saves $35,109 in total interest but requires $401 more initially each month.

Impact of Loan Term

Same amount and rate, different terms:

Conditions: $200,000 loan, 4.5% rate, Equal Payment

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 10 years | $2,073 | $48,712 |

| 20 years | $1,265 | $103,672 |

| 30 years | $1,013 | $164,815 |

Insights:

- 10 vs 30 years: $1,060 monthly difference

- But total interest is $116,103 more for 30 years

If affordable, shorter loan terms save significantly on total cost.

Calculating Effective Interest Rate

Don't just look at the nominal rate when comparing loan products.

Additional Costs to Consider

- Origination Fee: 0.2-1% of loan

- Title Insurance: For mortgages

- Appraisal Fees: Property loans

- Prepayment Penalties: May apply for early payoff

Compare the APR (Annual Percentage Rate) including these costs.

Loan Repayment Strategies

Strategy 1: Extra Payments

If you receive a windfall, consider prepayment. Reducing principal reduces future interest.

Example: $50,000 prepayment in year 5 on $300,000 loan

- Interest savings: Tens of thousands

- Check for prepayment penalties first

Strategy 2: Refinancing

If lower rate products become available, consider refinancing.

0.5% rate difference over 30 years is significant:

- $300,000 loan: 4% vs 3.5% = ~$28,000 difference in total interest

Strategy 3: Choosing Repayment Method

| Situation | Recommended Method |

|---|---|

| High, stable current income | Equal Principal |

| Want lower initial burden | Equal Payment |

| Goal: Minimize total interest | Equal Principal |

| Prefer easy monthly budgeting | Equal Payment |

Using the Repayment Schedule

Loan Calculator's repayment schedule feature shows:

- Payment-by-Payment Details: How much principal reduces each payment

- Break-even Point: When principal portion exceeds interest

- Prepayment Timing: When prepayment is most effective

Frequently Asked Questions

Q: How to calculate variable rate loans?

Calculate with current rate, then simulate rate change scenarios.

- Monthly increase if rate +1%

- Affordability if rate +2%

Q: What are DTI and DSR?

- DTI (Debt-to-Income): Mortgage payment vs income

- DSR (Debt Service Ratio): All loan payments vs income

Use Loan Calculator for monthly payment, then verify it's within 40-50% of income.

Q: What about grace periods?

During grace periods, pay only interest. After, principal payments begin and monthly burden increases suddenly. Plan accordingly.

Conclusion

If loans are unavoidable, understand them properly and use them wisely. With Toolypet's Loan Calculator:

- Simulate various rate/term combinations

- Compare Equal Payment vs Equal Principal

- Plan long-term with repayment schedules

Find optimal loan conditions for your situation.

Real-World Applications and Case Studies

Case Study 1: First-Time Homebuyer Decision

Michael is buying his first home and needs to choose between loan options:

Situation:

- Home price: $400,000

- Down payment: $80,000 (20%)

- Loan amount: $320,000

Option A: 30-Year Fixed at 6.5%

- Monthly payment: $2,022

- Total interest: $407,920

- Total paid: $727,920

Option B: 15-Year Fixed at 5.8%

- Monthly payment: $2,682

- Total interest: $162,760

- Total paid: $482,760

Decision: Michael can afford Option B's higher payment. He'll save $245,160 in interest and own his home 15 years earlier.

Case Study 2: Auto Loan Comparison

Sarah is financing a $35,000 car and receives two offers:

Bank A: 5.9% for 60 months

- Monthly: $675

- Total interest: $5,500

- Total paid: $40,500

Dealer Financing: 0% for 48 months (with $2,000 less trade-in)

- Monthly: $729

- Total interest: $0

- Effective cost: $37,000

Analysis: Despite the higher monthly payment, 0% financing saves $1,500 overall. Use Toolypet to compare all scenarios.

Case Study 3: Student Loan Payoff Strategy

David has $45,000 in student loans at 6.8%:

Standard 10-Year Plan:

- Monthly: $518

- Total interest: $17,160

- Total paid: $62,160

Accelerated 5-Year Plan (if affordable):

- Monthly: $885

- Total interest: $8,100

- Total paid: $53,100

- Savings: $9,060

Key Insight: Doubling the monthly payment doesn't halve the interest, but it still saves significantly.

Loan Calculation Formulas Explained

Equal Payment (Amortization) Formula

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Where:

M = Monthly payment

P = Principal (loan amount)

r = Monthly interest rate (annual rate / 12)

n = Total number of payments

Example: $200,000 at 5% for 30 years

- r = 0.05/12 = 0.00417

- n = 360 months

- M = 200,000 × [0.00417(1.00417)^360] / [(1.00417)^360 - 1]

- M = $1,074

Equal Principal Formula

Monthly Principal = P / n

Monthly Interest = Remaining Balance × r

Monthly Payment = Principal + Interest (decreases each month)

First month: $200,000 × 0.00417 + ($200,000/360) = $833 + $556 = $1,389 Last month: $556 × 0.00417 + $556 = $2 + $556 = $558

Total Interest Calculation

Total Interest = (Monthly Payment × n) - P

APR (Annual Percentage Rate) Formula

APR includes fees and represents true borrowing cost:

APR = 2 × n × I / [P × (n + 1)]

Where:

I = Total interest and fees

n = Number of payments

P = Principal

Frequently Asked Questions (FAQ)

Q1: Is it better to pay extra toward principal or invest the difference?

Compare your loan rate to expected investment returns:

- Loan at 4%: Investing may yield higher returns (historically 7%+ for stocks)

- Loan at 7%+: Paying extra provides guaranteed "return" equal to the rate

Consider also: Peace of mind from being debt-free vs. potential higher returns.

Q2: How does making bi-weekly payments help?

Bi-weekly payments mean 26 half-payments (13 full payments) per year instead of 12:

- Extra payment annually accelerates payoff

- $200,000 at 5% for 30 years:

- Monthly payments: 30 years to payoff

- Bi-weekly: 25.7 years to payoff (saves 4.3 years and ~$30,000)

Q3: What happens if I refinance mid-loan?

Refinancing resets your amortization schedule:

- Pros: Lower rate, lower payment, shorter term

- Cons: Restart paying mostly interest, closing costs, potential penalties

Calculate break-even point: When savings exceed refinancing costs.

Q4: How do adjustable-rate mortgages (ARMs) work?

ARMs have variable rates after an initial fixed period:

- 5/1 ARM: Fixed for 5 years, then adjusts annually

- Initial rates often lower than fixed rates

- Risk: Payments can increase significantly

Use Loan Calculator to model worst-case scenarios (rate + 2-3%).

Q5: What's the impact of credit score on loan rates?

Credit score directly affects offered rates:

- Excellent (750+): Best rates (e.g., 5.5%)

- Good (700-749): +0.25-0.5% higher

- Fair (650-699): +1-2% higher

- Poor (<650): +3%+ or denial

On a $300,000 loan, 1% rate difference = $50,000+ in additional interest over 30 years.

Loan Planning Checklist

Before Applying for a Loan

- Check and improve credit score if possible

- Calculate maximum affordable monthly payment (28% of income for mortgage)

- Compare rates from multiple lenders (at least 3)

- Understand all fees (origination, closing, prepayment)

- Calculate total cost of loan over its lifetime

Comparing Loan Offers

- Compare APR (not just interest rate)

- Calculate total interest paid for each option

- Consider loan term implications

- Factor in all fees

- Check prepayment penalty terms

Managing Your Loan

- Set up automatic payments (often get rate discount)

- Consider extra payments when possible

- Review refinancing opportunities periodically

- Keep records of all payments

- Monitor your remaining balance

Loan Comparison Tables

Mortgage Payment Examples ($300,000 Loan)

| Rate | 15-Year Monthly | 30-Year Monthly | 30-Year Interest |

|---|---|---|---|

| 5.0% | $2,372 | $1,610 | $279,767 |

| 5.5% | $2,451 | $1,703 | $313,212 |

| 6.0% | $2,532 | $1,799 | $347,515 |

| 6.5% | $2,613 | $1,896 | $382,633 |

| 7.0% | $2,696 | $1,996 | $418,527 |

Auto Loan Comparison ($30,000 Loan)

| Rate | 36-Month | 48-Month | 60-Month | 72-Month |

|---|---|---|---|---|

| 4.0% | $885 | $677 | $552 | $469 |

| 5.0% | $899 | $690 | $566 | $483 |

| 6.0% | $913 | $704 | $580 | $497 |

| 7.0% | $926 | $717 | $594 | $511 |

Total Interest on $30,000 at 6%:

- 36 months: $2,868

- 60 months: $4,800

- 72 months: $5,832

Summary: Making Smart Loan Decisions

Loans are powerful financial tools when used wisely. Understanding the math behind them empowers you to make decisions that save thousands over time.

Key Principles:

- Lower rates save more than shorter terms (usually)

- Equal principal saves interest but requires higher initial payments

- Extra payments accelerate payoff exponentially

- Always compare total cost, not just monthly payments

- Your credit score is worth protecting and improving

Using Toolypet's Loan Calculator:

- Compare repayment methods side by side

- Visualize payment schedules

- Calculate impact of extra payments

- Test different rate/term combinations

- Plan refinancing decisions

Action Steps:

- Enter your current or prospective loan details

- Compare Equal Payment vs Equal Principal

- Test shorter term scenarios

- Calculate total interest paid

- Make an informed decision

Remember: A loan is a long-term commitment. The time you spend calculating and comparing options with Toolypet can literally save you tens of thousands of dollars over the life of your loan.